XDI Announces Climate Risk Data on 34 million UK Addresses to Support Mortgage Lenders

4th November 2021

COP26, Glasgow

International climate change risk analysts XDI – The Cross Dependency Initiative – today released extreme weather and climate change physical risk statistics for all 34 million commercial and residential addresses in the UK. The report presents physical climate risk statistics including the geographical concentration of high-risk properties and the projected increases in insurance costs for 406 counties and equivalent areas.

Half a million high risk properties today, increasing to 1.9 million

The analysis suggests that climate exacerbated extreme weather risks may elevate insurance costs to unaffordable levels for many properties, leading to an increasing risk of financial distress and mortgage default. In some cases there are likely to be reductions in property value raising the spectre of negative equity.

Five fold increase in Technical Insurance Costs

Rohan Hamden, CEO said “Many large banks now have the capability to identify and therefore avoid addresses where extreme weather and worsening insurance costs could give rise to default risk. Without access to the same information, small and medium size lenders are potentially at risk of absorbing these assets, thus skewing the proportion of high risk addresses in their portfolio.”

Access to climate risk data for small and medium lenders

The release showcases the work of XDI’s Data Services Group, a new initiative to ensure climate intelligence is equally accessible to small and medium sized lenders and finance organisations. The announcement addresses an important risk to medium and small lenders as the UKs biggest banks finalise their risk analysis for the Bank of England CBES and may start to identify and avoid high risk addresses. XDI has been providing targeted analysis for large banks in the first round of BES reporting.

“Its very important that lenders get across the big picture numbers, but also the individual property risks so they know what they are taking on. This way they have the ability to advise the customers about alternatives or sensible adaptation options for their homes,” said Rohan Hamden.

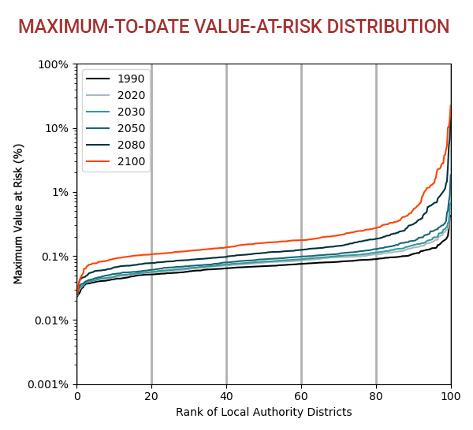

Distribution of MVAR across the areas for six time points

1.4% Property Value Corrections Overdue, 7.5% of climate correction projected

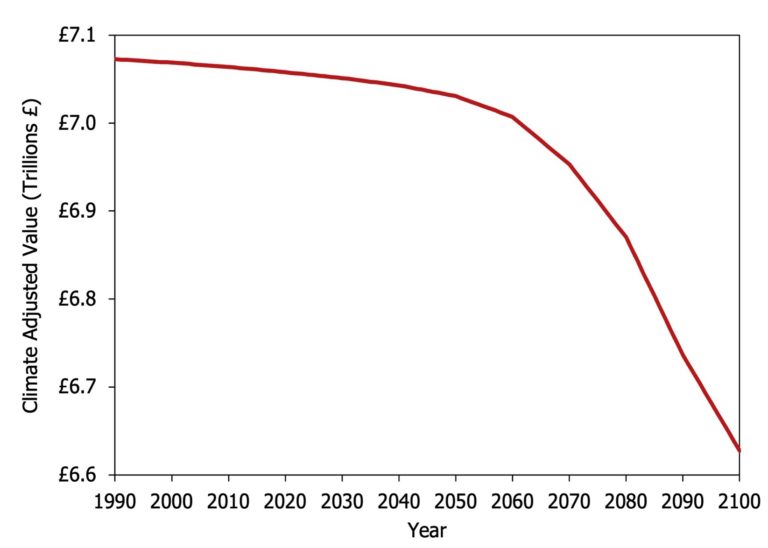

As both commercial and residential property buyers start to consider climate change and insurance costs in their purchasing decisions it is to be anticipated that properties highly exposed to extreme weather and climate change impacts will be decrease in value relative to the market. In some cases those declines may be severe enough to cause negative equity.

The modelling suggests an overdue market correction of 1.4% due to climate impacts

Looking forward, the decline will increase to 1.7% by 2050 and 7.5% by 2100.

Value of the likely correction is over half a trillion pounds (~ £525bn) before 2100.

Climate Adjusted Value over time of all UK addresses due to extreme weather and climate change impacts

Zero Knowledge system for simple security solutions

“A significant barrier in analysing mortgage portfolios is the need for banks to adhere to strong customer data security laws which make the cost of quality climate risk analysis prohibitive.” Said Rohan Hamden, “Our new solution uses a standardised zero-knowledge, double-encryption process which means that no customer information will leave the bank or lender. Consequently, high quality analysis will be within reach of the small to medium sized lenders.”

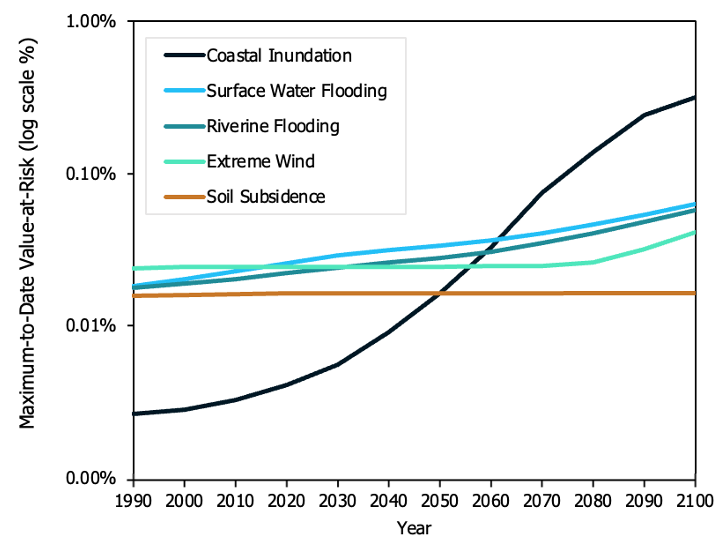

Inland flooding driving risk today, overtaken by coastal inundation as seas rise

Currently and in the short term, riverine and surface water flooding will be the main drivers of extreme weather and climate change impacts to property.

Eclipsed by coastal inundation driven by storm surge and sea level rise.

To a lesser extent wind storm events and soil subsidence during droughts represent lower level but widespread risk, which will be of less importance to lenders, but significant for insurers. The climate signal on these hazards is currently weak or uncertain.

Percentage properties flood exposed: 4% River, 7% surface, 6% coastal.

Change in Maximum-to-Date Value-at-Risk% over time due to each hazard

Recommendations

The report provides a series of recommendations to commercial and residential lenders including:

Assess risks to individual mortgage portfolios

Require comprehensive insurance coverage for high risk properties

Screen incoming mortgages at the point of sale

Be proactive with building resilience in the portfolio rather than relying on solutions from insurers or government

Develop climate-ready products and policies

Test adaptation strategies

Prepare for shareholder and RMBS scrutiny under TCFD

One of the biggest and most detailed climate physical risk analysis ever undertaken, encompassing 34 million addresses and 6 hazards across 110 years using engineering, weather, climate and hazard data in the purpose-built Climate Risk Engines software.

Climate change may have already increased extreme weather losses by an average of 18% since 1990.

The cost of insurance from extreme weather will increase 5-fold due to climate change by 2100 under a high-emissions (RCP8.5) scenario. Total Technical Insurance costs (annual average losses) increase from £2bn to over £10bn – in practice many such premiums will not be paid as they will be become unaffordable.

Properties with very high insurance costs will put mortgage serviceability under pressure and elevate the probability of default and negative equity.

Properties considered at ‘high risk’ of unaffordable insurance currently number 555,250 (or 1.6% of addresses) rising to 742,000 (2.18%) by 2050 and then to 1,860,000 (5.45%) by 2100.

Inland flooding (pluvial and fluvial) are the strongest drivers of risk today, but these will be overtaken by coastal inundation as sea levels rise (1.5m assumed by 2100 under RCP 8.5). Wind and soil subsidence impacts are widespread but not a default threat.

Flood exposed properties represent 4% of all addresses for riverine flooding, 7% for surface flooding and 6% coastal inundation.

Risks will be highly concentrated: 70% of the risks are confined to 20% of the 406 government areas analysed.

Lack of insurance is likely to be a trigger for lenders to refuse mortgages which, due to concentrations of impacts, may lead to some suburbs having an un-mortgageable property base.

The dataset is designed to assist lenders to quantify risks to their mortgage portfolio and to screen incoming mortgages for unacceptable risk.

Contact XDI to discuss Climate Change Physical Risk

XDI Cross Dependency Initiative provides physical climate risk analysis and reporting for financial service providers, business and government. We work with a wide range of government, business and financial sector clients including the British Columbian government, Legal and General Investment Management and Government of New South Wales. We work closely with approved resellers in the UK and North America to provide the physical risk component of TCFD reporting. XDI’s analysis uses multi-award winning technology and is proven in the market. XDI can provide asset level analysis and aggregated portfolio insights including failure probability, business disruption, supply chain risk and due diligence reporting.